Retirement Matters

June 2024

Solve the Social Security Deficit — In May, the most recent annual Social Security Trust Fund report said that unless changes were made, Social Security benefits would be cut by about 20 percent beginning in 2033. According to a February 2024 American Association of Retired Persons (AARP) survey, the importance of Social Security and Medicare to Americans age 50-plus cannot be overstated as 91 percent say Social Security is important when deciding their vote in elections, and 88 percent say the same about Medicare. In addition, nearly 90 percent of age 50-plus adults are worried that their Social Security benefits and Medicare benefits will be cut. More than 90 percent want Congressional Democrats and Republicans to work together to take action to extend the financial health of these programs.

It’s time to raise your voice to support those taking action to solve the Social Security deficit. Consider voting based on what’s critical for your financial security. Support Congressional representatives that take a leadership role, and make compromises to get things done, rather than holding out by stalling or opposing the needed legislation.

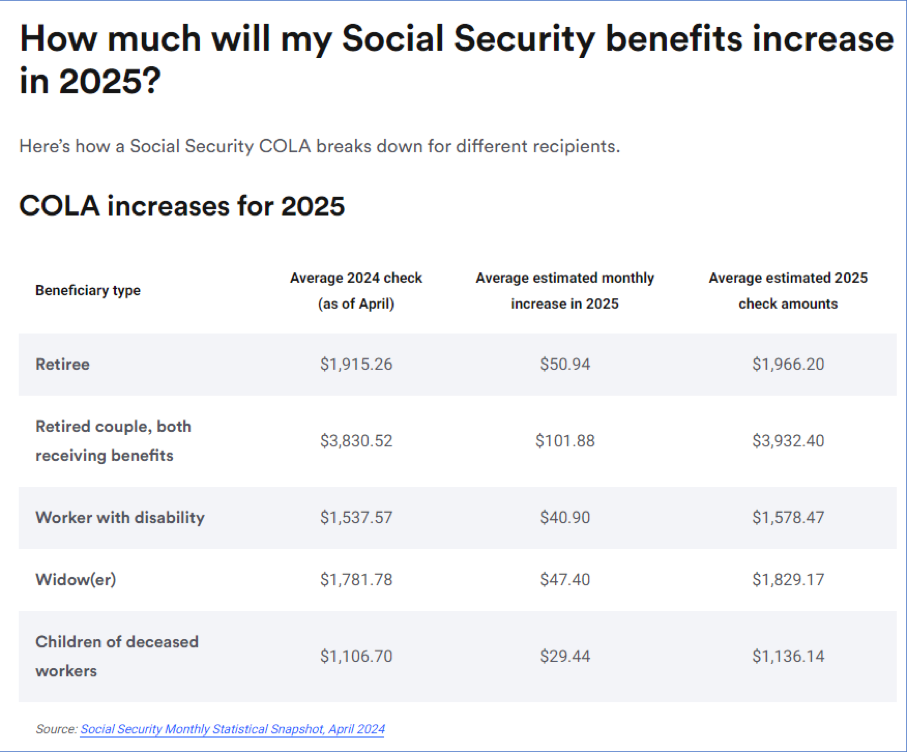

2025 Social Security Cost of Living Adjustment (COLA) Is Not Enough — The 2025 Social Security COLA will not be announced until October 2024, just a few months away. According to The Senior Citizen League (TSCL), a nonprofit and nonpartisan advocacy group, the Social Security COLA is estimated at 2.66 percent, starting in January 2025. This estimate is based on Consumer Price Index for Urban Wage Earners (CPI-W) through this April. With several months left until October, this estimate is likely to be adjusted. The final COLA provided in 2025 will be based on the average inflation rate in the third quarter (July, August, and September) of 2024, compared to the same months of 2023. See the “How much will my Social Security benefits increase in 2025?” chart with the increase based on your beneficiary type.

This COLA increase will not be enough to make ends meet for seniors collecting Social Security as their primary source of income. The TSCL 2024 Senior Survey, with over 1,100 responses, reported that seniors are struggling. It found that 71 percent of individuals said their household costs rose by more than the 3.2 percent COLA provided for Social Security in 2023. Many experts believe that the CPI-W doesn’t accurately reflect the impact of inflation on retirees, particularly when medical and health care costs are increasing rapidly. The TSCL survey indicated that 43 percent of those who responded reported their household expenses rose by over $185 per month in 2023. Within household expenses, 61 percent said their food expense increased the most. And 53 percent said they had spent their emergency savings. Using up your nest egg is a one-time solution. It’s not available to help shore up next year’s underfunded COLA.

2025 Medicare Premium Cost Increase — About 99 percent of Medicare Part A beneficiaries do not have a Part A premium because they have at least 40 quarters of Medicare-covered employment. Examples of Medicare Part A coverage include inpatient hospitals, skilled nursing facilities, hospice, and inpatient rehabilitation.

In March, the Medicare Trustees estimated a monthly Part B premium increase of about $10.30, from $174.70 in 2024 to $185 in 2025. Examples of Medicare Part B coverage includes physicians’ services, outpatient hospital services, home health services, and durable medical equipment. This premium increase is a burden to retirees living on fixed incomes at a time when they need relief from higher premiums and out-of-pocket health care costs. The increased Part B premium means those receiving Social Security will keep less of their COLA. We now turn from Social Security to the state pension plan.

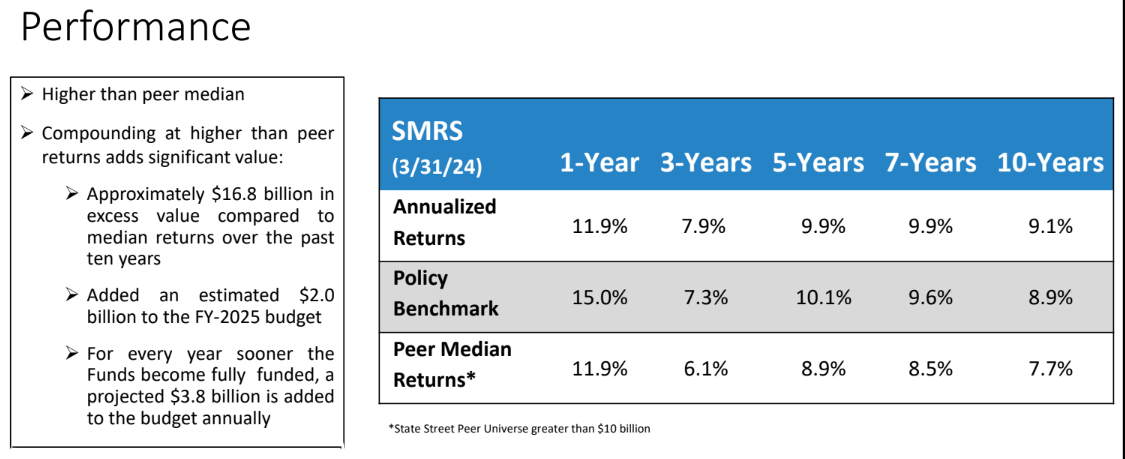

State of Michigan Investment Board (SMIB) — In June, Jon M. Braeutigam, Chief Investment Officer of the Bureau of Investments, discussed the performance of the State of Michigan Retirement System (SMRS), the combined retirement system that includes the State Employment Retirement System (SERS). The one-year return is 11.2 percent for the SERS total cumulative fund, as of 3-31-2024. The ten-year return is 9.1 percent for SERS, compared to a 7.7 percent 10-year return of its peers, which is made up of the State Street universe of public pension plans greater than $1 billion. See the “Performance” chart.

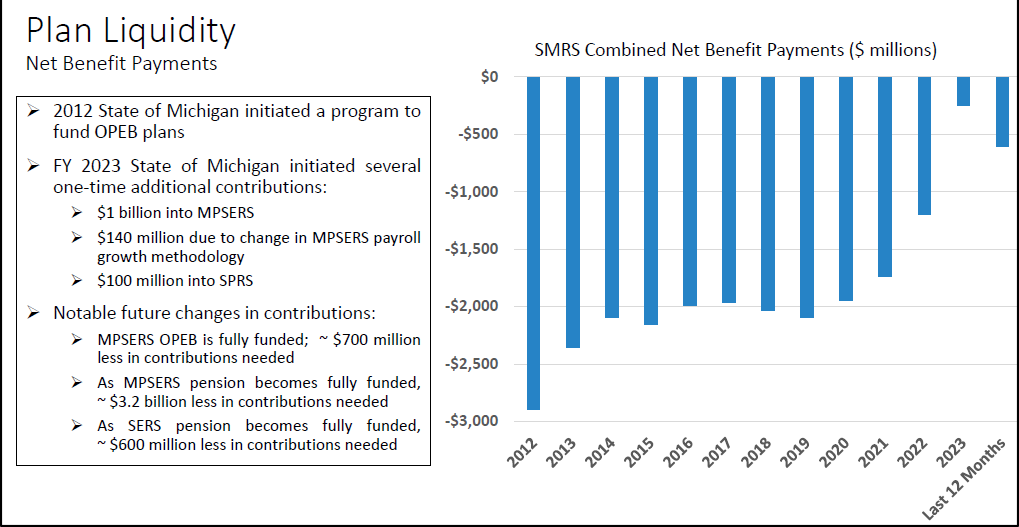

See the “Plan Liquidity” chart which identifies payments to Other Post-Employment Benefits (OPEB). These are benefits that employers provide to retirees, other than pensions, such as health care, prescription drug coverage, and dental and vision benefits. When the SERS pension becomes fully funded, an estimated $600 million will be freed up and could be used for other State purposes, given less in contributions are required. Also, in Fiscal Year 2023, large contributions were made to the Michigan Public School Employees Retirement System (MPSERS) so that its OPEB is now fully funded and requires about $700 million less in annual contributions.

Black Outs on the Rise — A recent study found that the number of major blackouts in the United States has more than doubled between 2015-16 and 2020-21. A dangerous illusion of extreme weather crisis is that we are smart and have modern life tools and technology that makes us invincible. The reality is that many don’t even have electricity or air conditioning. North Americans can expect frequent and prolonged power outages over the coming decade. Given these dire warnings, where are the advanced plans to save lives?

Are Utility Companies Doing Enough to Keep Us Safe? — If actions speak louder than words, probably not. DTE’s priority is to reward corporate executives by passing on private jet travel costs on to customers. In response, Michigan’s Attorney General Nessel is denouncing DTE’s $266 million request for a 10 percent gas rate increase, by 58 perent.

Similarly, Consumers Energy (CE) is now requesting a $303 million electric rate increase, effective in March 2025. This was requested just after the $92 million electric rate increase, down from $216 million originally, effective this March. The latest rate increase was based on a $7 billion Five-Year Plan that AG Nessel has criticized as lacking in affordability, reliability, and accountability. In the gas rate case, CE seeks a 37 percent increase in its residential monthly charge alongside a $136 million rate hike.

Editor’s note: Joanne Bump serves as feature columnist for “Retirement Matters.” Column content is time sensitive and is based on information as of 6/9/24. Joanne can be contacted by e-mail at joannebump@gmail.com.

Return to top of page