Retirement Matters

April 2024

At the SERA Lansing Chapter General Membership meeting on March 6, 2024, Anthony Estell, Director of the Office of Retirement Services (ORS), and Allison Wardlaw, ORS Plan Development and Compliance Director, presented an overview and improvements to the State Employees Retirement System (SERS) Defined Benefit (DB) and Defined Contribution (DC) plans.

DB Overview — The DB plan provides a monthly benefit for the retirees life which is determined by the age, years of service, and compensation. The benefit increases in proportion to the years of service. Pension plans accrue assets to provide pension benefits to retirees. The employer carries the risk for underfunding the plan.

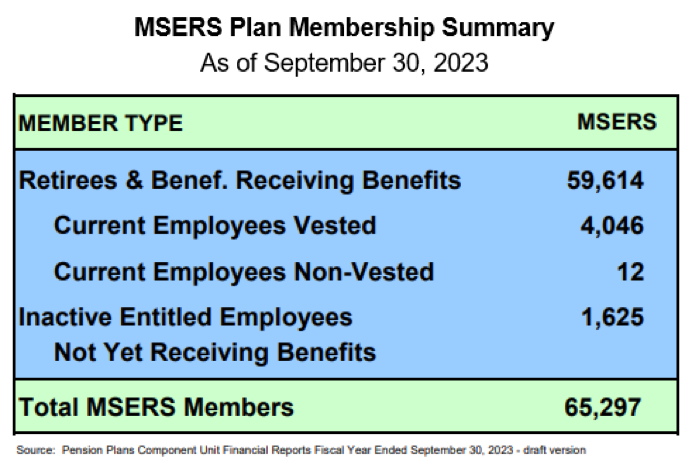

As the “MSERS Plan Membership Summary” chart below shows, 59,514 Michigan State retirees and beneficiaries are receiving benefits. Current or inactive employees have fallen to just 5,683 or 8.7 percent of the SERS members that may qualify for pensions in the future. In 1997, the DB plan was closed for State employees and the DC plan was introduced for newly hired State employees.

Pensions Primarily Funded by Investments — SERS is part of an overall Michigan State Retirement System (MSRS) that includes several retirement systems paying DB pensions to members from public schools, State employees, State Police, judges, military, Michigan legislators, and the Michigan National Guard. From every dollar paid in pensions, over 60 percent is financed from investment earnings (64 cents), followed by employer contributions (29 cents) and then (7 cents) from member contributions (National Institute on Retirement Security). Thats why its important to monitor the State of Michigan Investment Board reports

Improved Investment Practices have been implemented by the investment managers to align the investment assumptions with experience. These include:

- The Assumed Rate of Return (AROR) on investments typically has the largest effect of any assumptions on the liabilities and, therefore, required contributions.

- The Dedicated Gains Policy was adopted in 2017. When investment earnings exceed assumptions, the investment managers dedicate the excess investment gains to lower the AROR until it reaches a board-approved floor of 6 percent. The policy impact is that the Michigan retirement system liabilities will be more stable moving forward. As of September 30, 2023, the AROR for SERS is 6 percent for the pension and 6.2 percent for other post-employment benefits (OPEB), which are benefits other than pension distributions such as paid health insurance, life insurance, and deferred compensation.

- Five Year Experience Study - Investment assumptions are evaluated to see how closely they are matching actual experience. These assumptions are adjusted to reflect basic experience trends rather than random year-to-year changes. With each experience study, these actuarial assumptions should be more accurate representations of actual experience. (This discussion to be continued in upcoming SERA-Nades.)

DC Overview — The DC plan provides individual accounts, like a 401(k), for each retiree to accumulate assets for retirement. The individual can make voluntary contributions to their account. The employer makes contributions to the individuals account. The net retirement benefit is the balance in the account at retirement. The employee exclusively carries the risk of saving enough for retirement.

Designed for Success — The DC plan is administered by Voya Financial to provide the State of Michigan 401(k) and 457 plans with several low-cost investment choices. The plan is designed to help set up participants for success with features like automatic enrollment, a Small Steps Program, and Target Date Funds (TDF).

DC Match & Contribution — The State of Michigan begins contributing an amount equal to 4 percent of the employees pay into their 401(k) account. The State matches the first 5 percent of the employee contributions. These small percentages may not make or break your retirement savings, but consistent savings accumulation can provide a boost over time.

The DC State employee is automatically enrolled into a 401(k) Plan at a 5 percent contribution rate which is invested into a Target Retirement Fund (TRF) based on date of birth and an expected retirement age of 65. The first 3 percent of the employee contribution and State match is identified as retirement savings. The next 2 percent of both are for a Personal Healthcare Fund (PHF) that helps the employee pay for medical expenses in retirement. This is voluntary so the employee can change the contribution and investment options at any time. Overall, a significant 96.2 percent of the participants are taking advantage of the employer matching contributions.

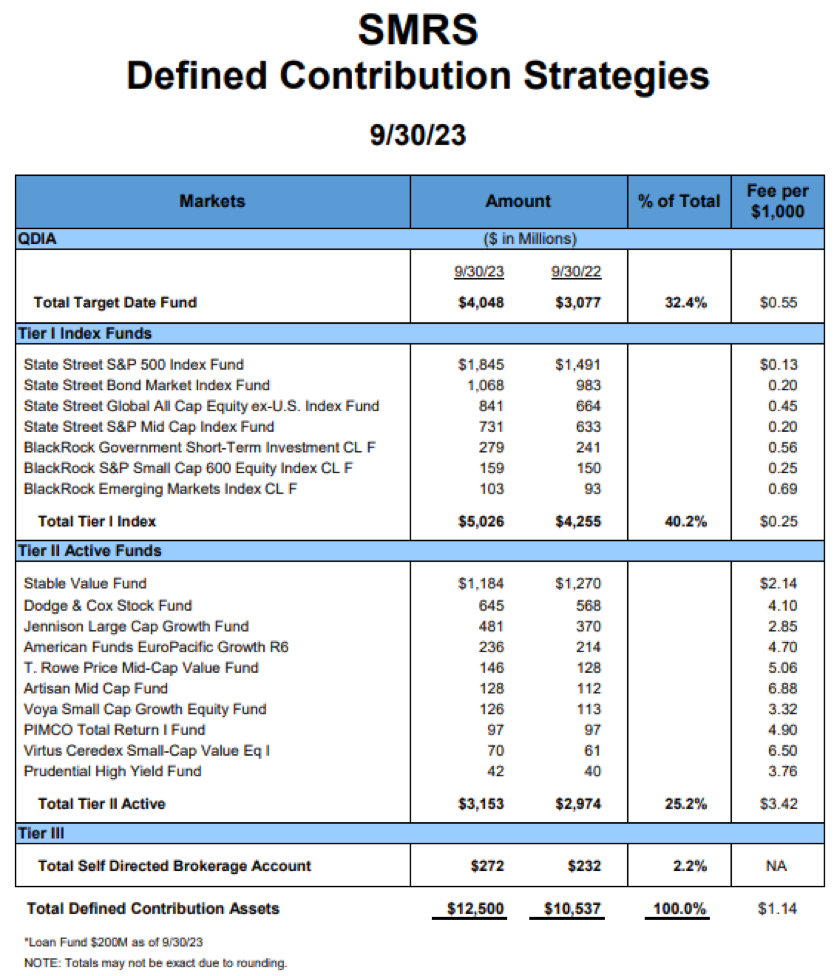

DC Investment Status — The “SMRS Defined Contribution Strategies” chart below illustrates total DC assets increased 18.6 percent from September 30, 2022, to reach $12.5 billion by September 30, 2023. This represents assets for the State of Michigans Retirement System (SMRS), as a whole, of which State employees are a part.

Notice that TDFs make up 32.4 percent of the total DC funds. TDFs include a mix of several different types of stocks, bonds, and other investments that are designed to take more investment risks when youre younger and gradually get more conservative as you near retirement, according to BlackRock, an investment manager. In addition, Tier 1 Index Funds make up 40.2 percent, Tier 11 Active Funds comprise 25.2 percent, and Self-Directed Brokerage Account encompass 2.2 percent.

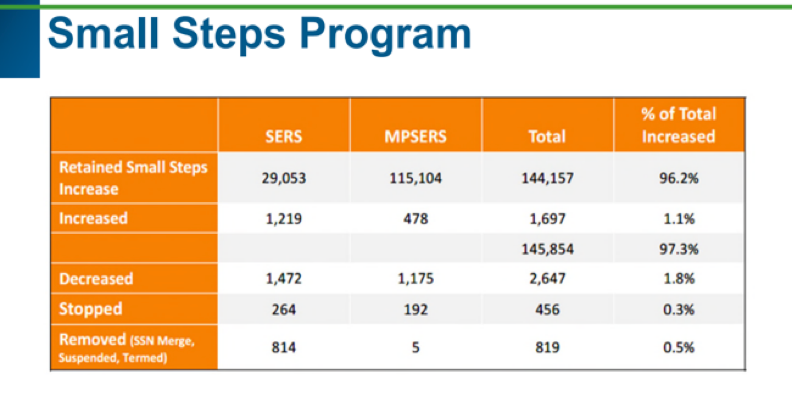

Small Steps Program — This DC plan increases the participant savings in meeting the match due in large part to the Small Steps Program (SSP) which is used to improve participant retirement readiness by gradually increasing employee contributions to their 401(k) and 457 plans by 1 percent each year (up to 15 percent).

There is a high level of participation in SSP from State employees. See the “Small Steps Program” chart below. Its important to note that the plan is voluntary, allowing some participants to opt out if the savings amount is too much for them to contribute. The chart shows only 7.8 percent of total employees participating decreased, stopped, or removed their contribution while 3.7 percent increased their contribution.

DTE Rate Increases — Michigans Attorney General Dana Nessel intervened in DTE Electrics most recent rate increase before the Michigan Public Service Commission. She calls the $450 million request, made just four months since the last one of $368 million, an oppressive rate hike not grounded in reality.

Editor’s note: Joanne Bump serves as feature columnist for “Retirement Matters.” Column content is time sensitive and is based on information as of 4/7/24. Joanne can be contacted by e-mail at joannebump@gmail.com.

Return to top of page