Retirement Matters

December 2023

Inflation Premium Increase — Long Term Care (LTC) insurance pays for nursing homes, assisted living facilities, and home care. Some State employee retirees received a letter in early November 2023 from Prudential LTC insurance notifying them that their daily maximum nursing home care and premiums were increasing. The premium increase may not affect every Prudential LTC insurance client. Prudential Insurance asked retirees to let them know in writing if they rejected the inflation protection increase. Your choices were to pay the premium increase, keep the previous premium that doesnt keep up with inflation and get lower benefits, or drop the LTC insurance.

Factors to Consider — LTC insurance protects your assets, the benefits are tax free, premiums are tax deductible up to a limit, and you can usually choose your caretaker. Drawbacks include the policy may not pay for everything you need, you may not qualify for the policy or benefits, and premiums may increase.

Most Americans want to avoid nursing homes and stay in their own homes, living independently for as long as they can. By 2030, one in five Americans will be at least 65 years old. With the growth of the aging population, seniors will compete for already scarce home health aides, nursing homes, and assisted living facilities. The Kaiser Family Foundation (KFF) survey reveals that families are already finding it difficult to get home health aides. Many cant pay what agencies charge, which is about $27 an hour, according to Genworth, a LTC insurance company. Untrained aides are found through informal, word of mouth channels. Due to the worker shortage, the waiting lists for aides is months long, so that many seniors only option is a nursing home.

Review whether you have a committed support group who could provide reliable unpaid help. As you age, a number of your trusted allies may not be able to help you because they have preceded you, are helping aging family already, or also have debilitating health conditions.

You cant depend on government to pay for most LTC expenses. Medicare or the federal health insurance for those 65 years and older, only pays for limited expenses. Medicare just covers short nursing home stays or limited amounts of home health care for situations like rehab after being in the hospital. Without LTC insurance, you have to pay for LTC care yourself if you need custodial care that includes supervision and assistance with day-to-day tasks.

Medicaid payments for LTC are limited to those that have low incomes and can show they hardly have any assets. Most State employees dont fall into this category until they have spent down their assets after a long nursing home stay.

Most senior Americans have not received the financial security they need to pay from private LTC insurance. For decades, the industry underestimated the number of policyholders that would use their coverage, how much longer they would live, and the high cost of their care. The industry is struggling, not selling policies, and leaving the market

Nursing Home Care Is Expensive! See the chart below for the average daily cost of a nursing home private or shared room. Compare the cost nationwide, Michigan statewide, and local areas like Lansing. Compare the new LTC insurance maximum daily nursing home rate of $311 to the Michigan statewide average. It doesnt cover your total daily cost for a private room of $324, so you would pay the rest yourself. It will cover the shared room rate of $299. Paying the LTC cost yourself requires readily available cash of over $109,000 a year for Michigans statewide average cost for a shared room. This cost is well beyond the ability to pay for most families.

Uncertain Who Pays? — The KFF recently published a survey showing that many Americans are confused about how LTC is financed. For those age 65 and older, 45 percent incorrectly assume that Medicare would pay the bill for a nursing home if they had a long-term illness or disability. In addition, four in ten adults mistakenly believe that Medicare, instead of Medicaid, is the primary source of insurance coverage for low-income people who need long-term nursing care. In addition, for most adults it would be very difficult or impossible to pay the over $100,000 needed for one year at a nursing home or $60,000 for one year for a paid nurse or aide. For the group of people 65 and older, 70 percent will need LTC.

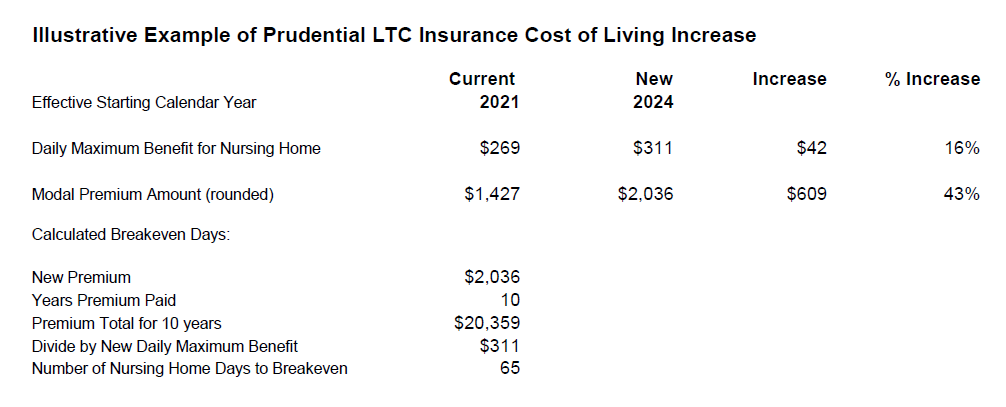

Illustrative Example — Its easy to dismiss the LTC premium increase of over 40 percent as too high. These LTC premium increases are not changed every year. The example shows the last increase occurred in 2021, with the new one representing an increase over three years. Based on the premium increase for an anonymous SERA member, the chart calculates the breakeven point for when the premium increase pays for itself in 65 days at a nursing home.

We do not have a crystal ball about how much LTC insurance we need. Each persons health and financial circumstances are different, so your calculation needs to account for those differences. Decide how much of your assets you want to protect with insurance by reviewing the recent value of your house, savings, IRAs, and annuities. New policies with the State of Michigan Group Prudential Long-Term Care Insurance were discontinued as of June 30, 2013, so State employee retirees have already been paying the premiums for at least ten years or more.

Look at the breakeven point to help you decide whether to accept the premium increase. Assume that you are age 65 and will pay the increased premium of $2,035.93 for at least the next ten years. Your cost to continue the insurance will be over $20,000 ($2,035.93 x 10 years = $20,359). You will use up or break even on the insurance premium within 65 days, or in just a little over two months. Over those years, the premium and daily rate will also rise. You dont want to accept a higher premium if you cant afford it.

Editor’s note: Joanne Bump serves as feature columnist for “Retirement Matters.” Column content is time sensitive and is based on information as of 5/7/23. Joanne can be contacted by e-mail at joannebump@gmail.com.

Return to top of page