Retirement Matters

October 2023

Health Care Crisis — If you or your family are experiencing long delays to get a medical appointment, you’re waiting a long time in the doctor’s office at your appointment, or the provider doesn’t answer the phone and you’re not sure the request will be answered, realize that you are not alone. It’s not the individual doctor or nurses’ fault as they are just a cog in the system. It’s because the nation has a health care crisis.

Most health care providers in the U.S. have a staff shortage and those left doing the work are burned out. During the Great Resignation in 2021-22, more than 5 million people left health care jobs in the U.S. The latest example of the crisis is shown by the Kaiser Permanente temporary work stoppage by 75,000 workers that ended October 7, 2023, without a deal. Wage increases aren’t the biggest problem for nurses and health care workers, but they care about how their work gets done.

Unfortunately, there isn’t a short-term fix. Up to two-thirds of health care staff are saying they are burnt out and more than one in five are quitting. These shortages are impacting all of us. The Emergency Care Research Institute (ECRI), an independent health care research firm, ranks the industry’s staffing shortage as the greatest risk to American patients. You can make a difference. Help your family and friends by calling early to get that health care appointment. If you don’t get an answer, keep calling back. Keep workers on the job by being patient and show your appreciation to the health care providers who are trying to serve you despite the shortage.

The State of Michigan Investment Board (SMIB) met September 28 to review the quarterly performance of the defined benefit (DB) and defined contribution (DC) plans for the combined Michigan retirement system, including Michigan’s State Employees’ Retirement System. State Street Global Advisers (SSGA) presented a report on the Defined Contribution and Target Retirement Strategy. The presenters included Mary Guy, Vice President Account Executive and Brendan Curran, CFA, and Managing Director, Head of Defined Contributions, Americas. They highlighted past trends and current performance of the State of Michigan DC plan to better inform the individual investors, like you, on the plan’s performance. SSGA is committed to advancing participant retirement readiness. This includes fiduciary oversight, recordkeeping support, public policy, product development, investment strategy, and participant engagement. This Retirement Matters column provided additional background information on definitions and the impact on Michigan’s State Employees’ Retirement System to promote your understanding of the trends. These investment trends and strategies are important to all current State employees and retirees.

The State of Michigan DC plan has grown to nearly $10.1 billion, based on its market value, as of June 2023. Over time, the market value of the DC plan has grown to more than six times the value of the State of Michigan DB plan. See the chart below. This isn’t surprising as the DB growth was curtailed by establishing a mandatory DC plan, instead of the DB plan, for State employees hired after March 1997, over 2 ½ decades ago.

Michigan Department of Treasury

Invetment SummaryAs of June 30, 2023: |

|

| Market Value ($) | |

| State of Michgian Defined Contribution | 8,679,330,422 |

| State of Michgian Defined Benefit | 1,411,351,058 |

| Total | 10,090,681,480 |

Source: SSGA

(Includes dividends, interest, and realized/unrealized gains and losses.)

The disadvantage of relying on the DC plan for new hires is that the employee may not have as much money for retirement as they may have had if the employer provided a DB plan with professional investors. Since the employee is making investment decisions, it can be risky, as many individuals lack knowledge on investing.

Further, the passage of the Pension Protection Act (PPA) of 2006, had the inadvertent consequence of making the U.S. retirement financing predicament even worse, according to the National Institute on Retirement Security. With changing and less workable funding rules in the law, employers were less willing to sponsor DB pension plans.

2023 DB Decline — The State of Michigan DB account changes have declined from $1.57 billion to $1.41 billion from January 1, 2023, to June 30, 2023. This decline in the first half of 2023 is primarily accounted for by withdrawals, needed to pay pensions, of over $300 million and appreciation/depreciation of nearly $139 million. See the chart below.

Michigan Department of Treasury

Statement of Asset ChangesThe following changes took place in the State of Michigan Defined Benefit account from January 1, 2023 to June 30, 2023: |

|||||

| Starting Balance 01/01/23 ($) |

Contributions ($) | Withdrawals ($) | Appreciation/ (Depreciation)* ($) |

Endeing Blanace 06/30/2023 ($) |

|

| State Street MSCI ACWI Ex USA Index SL Fund | 1,572,490,377 | 44 | (300,017,460) | 138,878,07 | 1,411,351,058 |

| Total | 1,572,490,377 | 44 | (300,017,460) | 138,878,07 | 1,411,351,058 |

Source: SSGA

(Includes dividends, interest, and realized/unrealized gains and losses.)

Significant DC Growths — Michigan’s DC growth is in keeping with U.S. trends outlined by SSGA showing that DC plans have realized strong historical growth in response to investment trends. The chart below shows the U.S. public sector segment of DC plans grew by over 62 percent from $1,815 billion in 2016 to $2,942 billion in 2021.

Target Date Funds (TDF) Use Risess — The use of TDFs and index funds has grown significantly after the passage of the PPA of 2006. TDFs are used to save for retirement, with investors selecting a target date fund based on their target retirement date. As investors get closer to the time that they want to start using their savings for income, they need to protect more of their money from losses. They become more conservative by changing the mix of assets to increase their allocations to bonds or cash equivalents. In addition, TDFs focus on growth with higher fees than the more passively managed funds typically available with 401(k) plans. TDFs come with fee structures, while index funds typically charge little due to their passive management.

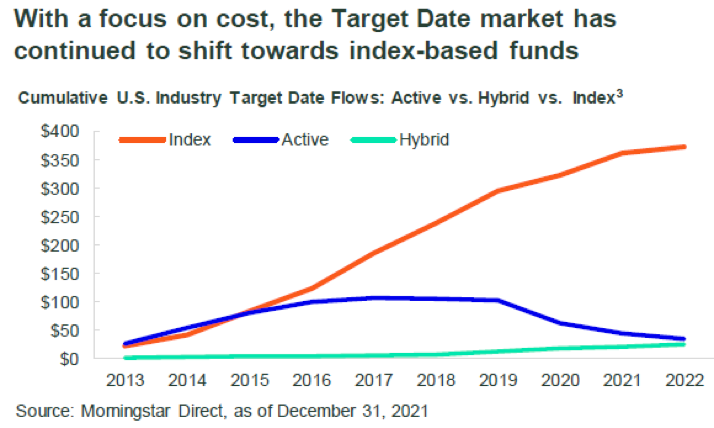

Index Fund Usage Ups — With a motivation for lowering costs, the TDF market has continued the shift towards index-based funds. The TDF flow to index funds has steadily grown from 2013 to 2022. See that the chart’s index fund line significantly outpaces the growth of hybrid and active plans through 2022. Active funds are managed and try to beat market returns with investments hand-picked by professional money managers. Hybrid funds contain elements of both defined benefit and defined contribution plans.

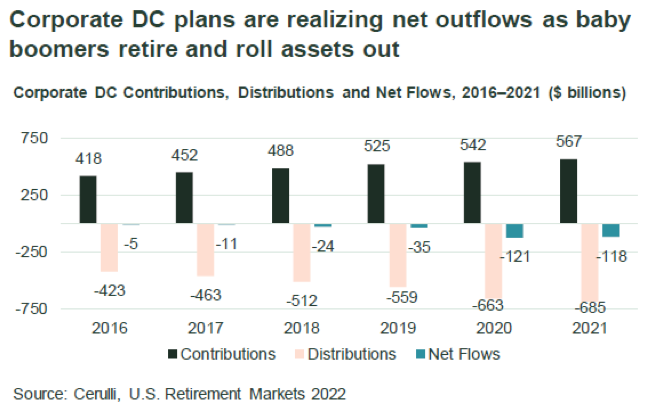

Baby Boomers’ Withdrawalss — Corporate DC plan contributions have continued to grow in recent years. However, the net outflows are increasing as retirees make withdrawals to fund baby boomer retirements for those born between 1946 and 1964. As shown in the chart below, the growing net decline of Corporate DC contributions vs. distributions has risen from -$5 billion in 2016 to -$118 billion in 2021.

Balance Risks in Retirements — SSGA recommends that investors balance key risks in retirement. Participants efficiently address market, inflation, and longevity risks by implementing the objectives listed below and investing in a diverse mix of asset classes.

- Grow retirement savings to mitigate accumulation risks.

- Reduce volatility to preserve accumulation savings.

- Protect purchasing power from Inflation.

- Maintain growth for an increasing lengthy retirement.

Editor’s note: Joanne Bump serves as feature columnist for “Retirement Matters.” Column content is time sensitive and is based on information as of 5/7/23. Joanne can be contacted by e-mail at joannebump@gmail.com.

Return to top of page