Retirement Matters

June 2023

Save SERA — Recently, SERA successfully advocated for the repeal of the pension tax on State employee benefits. We have received many thanks for our effective influence. However, we have more vital work to do like maintaining retirees’ pensions and health care benefits which are being eroded by inflation and bad policy choices. In addition, the “Retirement Matters” column informs our members on federal policy trends that could affect their Social Security and Medicare benefits. Our work requires a strong membership and advocacy organization. However, membership recruitment has become difficult as the State government has stopped providing SERA with retiree phone numbers, or home and e-mail addresses due to privacy concerns within the Freedom of Information Act. SERA has written to and met with State policy makers asking for the return of contact information without results. We are hopeful that we can get this situation resolved. As a stop gap, we need your help to reduce costs.

Volunteer Today — Most of SERA’s cost is devoted to publishing the SERA-Nade newsletter including printing and postage. Understandably, some retirees are not able to use an e-mail to receive the newsletter. But, for those of us that read directly from our computers, please volunteer to convert your U.S.-mailed paper copy to the same professional looking newsletter, but in a PDF version that’s attached to your e-mail. Please e-mail Sara Gross at seramembership@yahoo.com and ask for the e-mailed newsletter instead. Or, check the box that says “I wish to receive the SERA-Nade by e-mail” on the SERA-Nade membership renewal form.

State of Michigan Retirement Board (SMRB) — On May 11, 2023, the board met to present findings from the annual actuarial reports on the State Employee Retirement System (SERS) for our pension and health care funds. This report was prepared by Gabriel, Roeder, Smith & Company (GRS) and based on September 30, 2022, data, which is the latest available. SMRB also presented a March 23, 2023, summary of the Michigan Department of Treasury, Bureau of Investments conclusions.

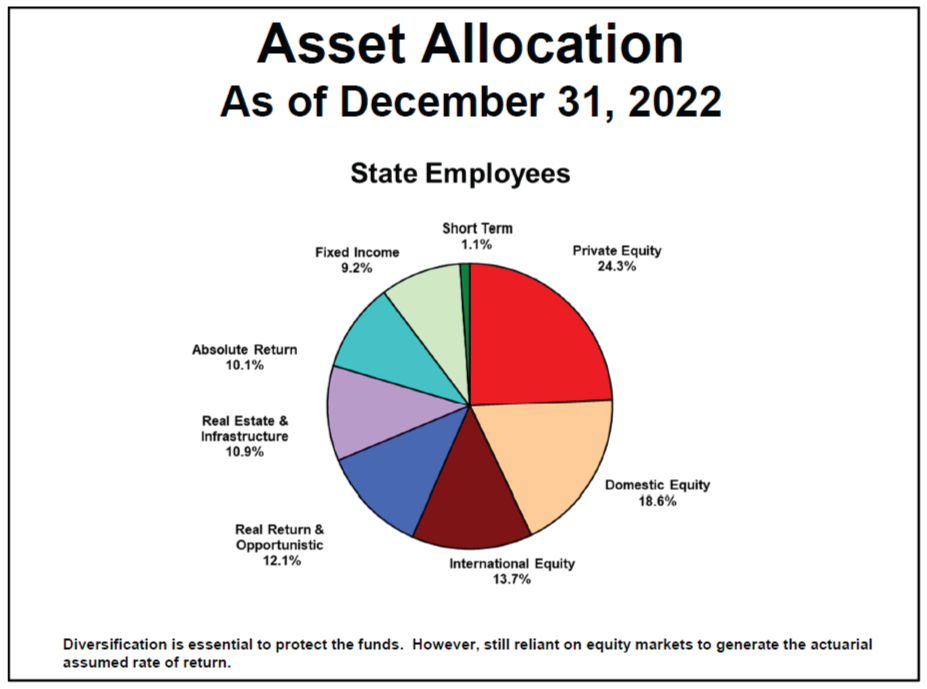

Dedicated Gains Policy — The purpose of the Pension Actuarial Valuation Results report is to determine the employer contribution for Fiscal Year 2025 and to measure the system’s funding progress. Industry experts are predicting lower returns for the next ten years. Thus, most plans are lowering their actuarial assumed rate of return. This means that the asset allocation will change to more secure investments that earn a lower rate of return. See the 2022 SERS Asset Allocation chart. Michigan has also placed a floor on the return assumption with a dedicated gains policy that was adopted by the Board of Trustees, starting with the September 30, 2021, funding valuation. This policy prevents lowering the SERS pension investment return assumption below 6 percent, meaning pension investments are assuming some level of risk.

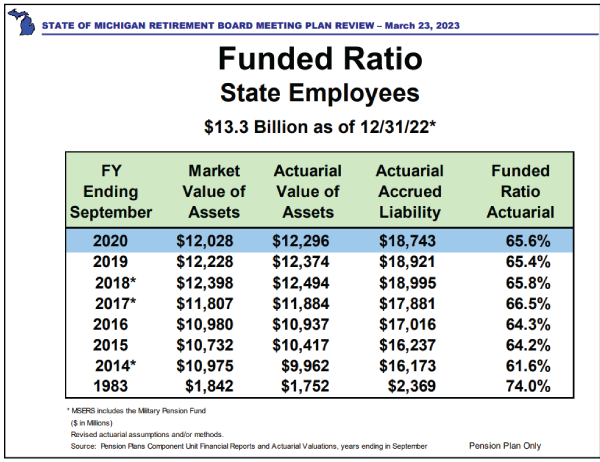

Fund Ratio — Like most states, Michigan has not completely funded the public pension systems but is working toward that direction. The value of pension assets has benefited from significant long-term investment growth. The 2022 Pension Annual Actuarial report for SERS shows how much of the State employee pension costs are fully paid up. It gauges the health of a defined benefit pension plan and whether the fund has enough to pay out pensions. The SERS “fund ratio” is the pension plan’s assets as a percent of liabilities on an actuarial basis. From 2017 to 2020, Michigan’s fund ratio has consistently hovered over 65 percent. See the SERS Funded Ratio chart with a historical trend in funded ratios through 2020. The funded ratio continued to rise to over 69 percent in 2021 and 2022.

SMRB Conclusions — In 2022, the highest rates of inflation were recorded since 1982 with Federal Funds interest rates remaining around 0 percent. The inflation rate reached its highest rate over the period and then slowed down. The SMRB plans to continue maintaining a long-term perspective with adequate cash, or liquidity, to pay pensions during these short-term market changes.

Pension Increase — The SERS average annual pension rose slightly from $24,131 in 2021 to $24,598 in 2022, up a mere 1.9 percent. By comparison, Michigan’s actual Detroit CPI (consumer price index) in 2022 was 7.9 percent or 4 times larger. This illustrates the large unpaid pension gap for State employee retirees which will continue into the future.

$300 Cap — This low 1.9 percent pension growth rate for 2022 reflects the policy impacting over 80 percent of State employee retirees that don’t receive the full 3 percent COLA (cost of living adjustment) on the retirees’ base income (cumulative not compounded) on the date of retirement because they have reached the $300 cap on annual increases for defined benefit State retirees. This outdated cap, in place since 1987, should have been indexed to inflation but was not.

In 2023, elevated inflation rates will continue, but are moderating. Michigan’s CPI is forecasted to fall to near more normal levels of 3.1 percent for Fiscal Year 2023, according to the May 2023 Michigan Consensus Economic Forecast. In 2023, the Federal Reserve is managing inflation by increasing interest rates, but weighing the risk of a hard landing becoming too great.

Medicare Drug Prices — In early June, Merck, the pharmaceutical company, sued the government over a federal law giving Medicare the power to negotiate prices directly with the drugmakers. Merck made $14.5 billion in profits last year but is asserting that the new law would hinder its ability to make risky investments. This provision was included in the Inflation Reduction Act of 2022 giving Medicare the ability to lower drug prices. It will make prescription drugs more affordable for seniors with diabetes, cancer, respiratory conditions, or cardiovascular diseases. Merck is asking for a court order that would exempt them from the negotiation program, claiming it’s unconstitutional. This is Merck’s first attempt to challenge this significant revision to health care policy before it goes into effect in 2026. But some experts claim that the constitutionality arguments are weak and they would face a push back in court. Hopefully, the Biden administration will prevail in their plan to forcefully defend the law.

Editor’s note: Joanne Bump serves as feature columnist for “Retirement Matters.” Column content is time sensitive and is based on information as of 5/7/23. Joanne can be contacted by e-mail at joannebump@gmail.com.

Return to top of page