Pension Matters

State Employees Retirement Fund

Most Recent Market Value | Michigan Treasury Bureau of Investments

June 2017

Social Security Increases Security

Starting June 10, the Social Security Administration will require you to choose a second identification method to log into your My Social Security online account. You’ll have to provide a cell phone number or an e-mail address; a one-time security code will e sent as a text or email each time you log into your account. You’ll have to plug in the code to access your account.

Funding State Pensions

A recent article in the Detroit News says, “The state employee pension system has compiled nearly $6 billion in debt or ‘unfunded liabilities’ in the 20 years after legislators ended state employee pensions for new hires in 1997. The state employee system was fully funded in 1996 when then-Gov. John Engler and the Republican-led Legislature finalized a groundbreaking move to shift new hires into 401(k)-style retirement savings plans.” Read more at www.detroitnews.com

I Couldn’t Have Said it Better

“There is nothing inherently wrong with pension systems the problem is that politicians simply don’t fund them and instead pass the costs of today’s government onto future taxpayers.” Jarrett Skorup of the Mackinaw Center.

Getting Rid of Pensions at any Cost

Making newly hired teachers and other school employees ineligible for a pension and instead giving them a 401(k) would cost Michigan $465 million more annually in the first five years, according to an analysis by the House Fiscal Agency. (See Legislative Analysis of House Bill 4647)

Funding Levels for Largest US Pension Plans

A report by Milliman Public Pension Funding group annually explores the funded status of the 100 largest U.S. public pension plans. Milliman is listed as one of the world’s largest providers of actuarial services.

Highlights

- As of June 30, 2016, the aggregate funded ratio is estimated to be 69.8

- Plan sponsors continue to reduce interest rate assumptions in the expectation that returns over the coming decades will be lower

- The difference between the average sponsor-reported assumption of 7.50% and our independently determined assumption of 6.99% is the highest we have seen, indicating that pressure to reduce interest rate assumptions is unlikely to abate”

Of the 100 plans analyzed, 15 had funding ratios above 90%, 64 between 60% and 90%, and 21 below 60%. As of Dec. 31,2017 10 plans had funding ratios above 90%, 65 between 60% and 90%, and 25 below 60%”

You can find the full study at www.milliman.com/ppfs to see where Michigan ranks.

The “New Retirement” Strategy That’s Gaining Popularity

Recent studies have shown that the impulse to file for Social Security benefits at the earliest possible age (62) is giving way to deferred filing, either at the full retirement age (66/67) or even up to age 70. Whether that’s because of a better understanding of the long-term impact of early retirement penalties or the efforts of many to dispel the rumors that the Social Security program will “soon” vanish is subject to debate, but Fidelity’s Social Security IQ shows that the number f those planning to file at 62 is dropping near the one-quarter mark. Further, the survey found that “the percentage of people 65 and older who still work has also been climbing.” The combination of these two mindsets — delayed filing and a longer working lifewill certainly improve the future financial lives of many retirees. Posted: 11 May 2017 06:09 AM PDT Read more about this trend in a CBS NEWS article posted on www.wsaw.com.

Couldn’t Have Said it Better

“Defined-benefit pensions could work just fine for both employers and employees. But government pensions have a major problem: They are ultimately run by politicians who are good at and used to making promises, but also good at and used to passing the bill to somebody else The consequences of failing to pay the true cost of these promised pensions occur decades into the future, so it’s very easy for politicians to just push the burden onto future taxpayers.“ Posted by James M. Hohman on May 16, 2017 at 12:30pm

Read the entire article at www.mackinac.org

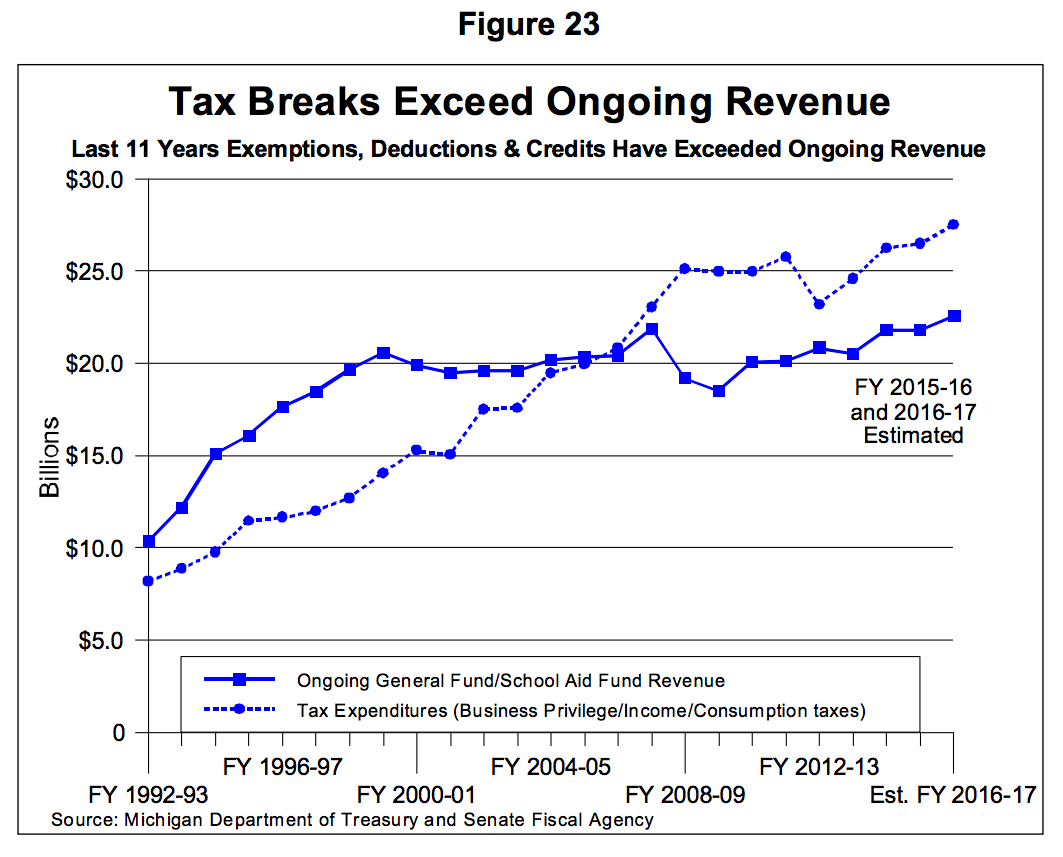

Revenue Estimates Looking Good

According to a news release from Treasury, “State Treasurer Nick Khouri, State Budget Director Al Pscholka, Senate Fiscal Agency Director Ellen Jeffries and House Fiscal Agency Director Mary Ann Cleary today reached consensus on economic and revenue figures for the remainder of Fiscal Year (FY) 2017 and for the upcoming 2018 and 2019 Fiscal Years.

Following today’s Consensus Revenue Estimating Conference, net FY 2017 General Fund-General Purpose (GF-GP) revenue is projected at $10.1 billion, down $178.8 million from estimates agreed to in January. Net FY 2017 School Aid Fund (SAF) revenue is now estimated at $12.6 billion, up $152.9 million from January. Combined, GF-GP and SAF estimates are down approximately $25.9 million for FY 17.”

You’ll Need More Retirement Income Than You Think

According to the Employee Benefit Research Institute (EBRI), “46% of households spend more money, not less, during the early years of retirement. For 33% of households, this trend lasts a solid six years. And roughly 25% of households wind up needing more than 120% of what they previously spent each year prior to retirement. When you think about giving up that weekly takeout order or annual vacation to buy yourself more financial freedom in the future, remember that doing so might end up being a matter of survival.“ Read more at www.fool.com.

Bureau of Labor Report — December 2016

The U.S. Bureau of Labor Statistics reported recently that employer costs for employee compensation averaged $34.90 per hour worked in December 2016. Wages and salaries averaged $23.87 per hour worked and accounted for 68.4 percent of these costs, while benefits averaged $11.03 and accounted for the remaining 31.6 percent.

- Total employer compensation costs for private industry workers averaged $32.76 per hour worked in December 2016.

- Total employer compensation costs for state and local government workers averaged $47.85 per hour worked in December 2016.

Read more at www.bls.gov

Annual Statistical Supplement to the Social Security Bulletin, 2016 — Worth a Look

The Supplement includes more than 200 statistical tables that provide data on Social Security and Supplemental Security Income. The data cover program details such as beneficiary counts, amounts of benefits, and the status of the trust funds. You can find this information at www.ssa.gov.

FYI

Editor’s note: June Morse may be contacted at jmorse10@comcast.net or 517-886-9323.

Return to top of page