Pension Matters

State Employees Retirement Fund

Most Recent Market Value | Michigan Treasury Bureau of Investments

February 2016

Bureau of Investments (BOI) Presents at SERA Meeting

Jon Braeutigam, Chief Investment Officer and Robert Brackenbury, Senior Director of Investments gave us an update on the State Employees Retirement System (SERS) Pension Fund. The Bureau of Investment, in the department of Treasury, has more than $78 billion under its management, $12.2 billion is the State Employees’ Retirement System. BOI operates with 79 full time employees. There are a total of 76,463 total members in the SERS, 58,453 are current retirees and beneficiaries receiving benefits. For 2014, the market value of the SERS was 61.6% (smoothed) with a calculated market value funded ratio of 75.2%.

Mr. Braeutigam explained that the fund is“broadly diversified” with emphasis on reaching or surpassing the 8% factor. The funds rate of return for over 3,5, and 7 years has been well above the 8%. Michigan’s retirement plan has been called one of the“best performing plans in the nation.“

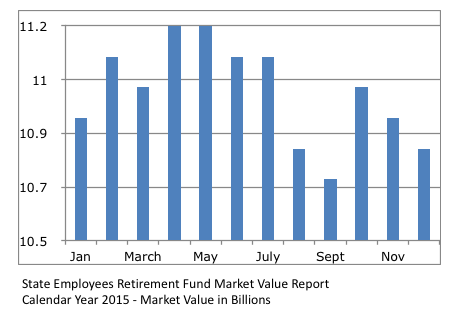

The chart below shows the SERS funds market value for the 2015 calendar year.

How did your portfolio perform last year? According to market watchers, all you had to see was a 1% rise to do better than the S&P 500 , which was down 0.7% at the end of 2015. You can find detailed quarterly investment reports for all State retirement systems on Treasury’s web site at www.michigan.gov/treasury

How did your portfolio perform last year? According to market watchers, all you had to see was a 1% rise to do better than the S&P 500 , which was down 0.7% at the end of 2015. You can find detailed quarterly investment reports for all State retirement systems on Treasury’s web site at www.michigan.gov/treasury

Simplifying Choices in Defined Contribution Retirement Plan Design

Donald B. Keim, Olivia S. Mitchell, NBER Working Paper No. 21854, Issued in January 2016

Abstract:“In view of the growth and popularity of defined contribution pensions, along with the government’s growing attention to retirement plan costs and investment choices provided, it is important to understand how people select their retirement plan investments. This paper shows how employees in a large firm altered their fund allocations when the employer streamlined its pension fund menu and deleted nearly half of the offered funds. Using administrative data, we examine the changes in plan participant investment choices that resulted from the streamlining and how these changes might affect participants’ eventual retirement wellbeing. We show that streamlined participants’ new allocations exhibited significantly lower within-fund turnover rates and expense ratios, and we estimate this could lead to aggregate savings for these participants over a 20-year period of $20.2M, or in excess of $9,400 per participant. Moreover, after the reform, streamlined participants’ portfolios held significantly less equity and exhibited significantly lower risks by way of reduced exposures to most systematic risk factors, compared to their non-streamlined counterparts.” To read the full article, go to www.nber.org

Just so you Know

“Earlier claiming by men and women, which results in smaller monthly Social Security checks, has fallen especially hard on elderly widows. After a husband dies, the two benefit checks coming into the house are reduced to one. Although widows receive the larger of the couple’s two checks — typically the husband’s — it may not be sufficient to maintain her standard of living.” Read more at http://squaredawayblog.bc.edu

AARP Booklet on Benefits for Seniors in Michigan

AARP Foundation has put together a comprehensive file for persons 50 years of age or older, who need resources to help with issues of hunger, isolation, income, and housing. Complete PDF file at www.aarp.org

Program guidelines, telephone numbers, and Web sites are subject to change. For the most up-to-date information log on to Benefits QuickLINK at: http://www.aarp.org/quicklink.

Does a Uniform Retirement Age Make Sense?

The Center for Retirement Research at Boston College has posted a new brief on retirement age. Due to enhanced life expectancy, some experts would want people to work longer. However, that concept does not fit all. “Policymakers seeking to encourage working longer should be cautious about the potential effects that such policies could have on inequality.” Read more at http://crr.bc.edu

Helpful Definitions

When seeking financial advice consider the following:

Investment Advisers — paid to give advice. Held to a fiduciary standard (put your interests above their own) Find registered investment advisers at www.adviserinfo.sec.gov

Brokers — buy and sell stocks, bonds, etc. No fiduciary requirement. Must be registered and licensed. Check out a broker’s background at http:///brokercheck.finra.org or contact the state’s securities regulator.

Financial Planners — may use the title advisor or broker or have no credentials. Check out education and certification requirements at www.finra.org.

(Kiplinger’s Retirement Report, February 2016)

Tax Information

You can deduct more of your long term care insurance premiums as a medical expense in 2016. Taxpayers 71 and older can claim up to $4,870; age 61-70, up to $3,900 and those 51-60 can claim up to $1460. (Kiplinger, 2-16)

If you adjusted gross income for 2015 is $62,000 or less you can file your federal tax free using Free File Alliance. Learn more at www.irs.gov/freefile

Editor’s note: June Morse may be contacted at jmorse10@comcast.net or 517-886-9323.

Return to top of page