Pension Matters

State Employees Retirement Fund

Most Recent Market Value | Archived Monthly Profiles

March 2013

2012 Comprehensive Annual Financial Report (CAFR) is Online

Highlights

- As of September 30, 2011 funded ratio was 65.5% and the funded ratio of post-employment benefits 0%.

- As of September 30, 2011, the actuarial accrued liability for post-employment benefits based on pay as you go is $14.3 billion. If these benefits were pre-funded, the actuarial accrued liability as of September 30, 2011, would be $8.8 billion.

- System assets exceeded liabilities at the close of fiscal year 2012 by $9.6 billion (reported as net assets).

- Additions for the year were $2.5 billion, which are comprised primarily of contributions of $1.2 billion and investment gains of $1.3 billion.

- Deductions increased over the prior year from $1.6 billion to $1.7 billion or 5.4%. Most of this increase represented an increase in pension and health benefits paid.

- System assets exceeded its liabilities at the close of fiscal year 2012 by $9.6 billion. Net assets held in trust for pension and OPEB benefits increased $841.5 million or 9.6% between fiscal years 2011 and 2012 due primarily to increased investment income. Total net assets decreased $265.2 million or 2.9% between fiscal years 2010 and 2011 due primarily to investment losses.

Raleigh Studio

“The Michigan Department of Treasury - Bureau of Investments reported a cumulative probable loss of $20.0 million in fiscal year 2012 related to the guarantee of bonds for a Michigan motion picture studio. The System’s proportionate share of this loss is 19.2% or $3,833,824 and is reported as an administrative and other expense on the Statement of Changes in Pension Plan and Other Postemployment Benefit Plan Net Assets for the fiscal year ended September 30, 2012.”

Actuarial Assumptions

Rate of return used was 8%; long term real rate of return is 4.5%.

Expenses

Investment Expenses for 2011 - $35,479.170; for 2012 - $35,866,062

Professional Services for 2011 - $1,287,182 for 2012 - $1,136,726

The full report is posted at the Office of Retirement Services website at www.michigan.gov/orsstatedb and click on the green tab on the right. (Thanks to Dave Berquist for the heads up)

Retirement Plans FAQs regarding Required Minimum Distribution (RMD)

The IRS has put out a Q&A regarding RMD which you may find helpful in making decisions about this required withdrawal from pre tax retirement contributions. You can find this site at www.irs.gov/Retirement-Plans/Retirement-Plans-FAQs-regarding-Required-Minimum-Distributions#1

How much is saved in 401(k)?

Fidelity Investments’ quarterly analysis of 401(k) plans found that participants, on average, save 8 percent of their annual salaries in their 401(k) plans, and when the typical employer contribution is factored in, be it a match or profit sharing, the average participant’s total savings rate increases to 12 percent. For a 15th straight quarter, more participants increased their savings rate than decreased it (5.8 percent vs. 3.1 percent). Fidelity notes that 37 percent of work place retirement plans offer a Roth savings option, up from 12 percent five years ago. Of these plans, 12 percent offer the Roth in-plan conversion option. Roth contributors boast a higher savings rate, deferring an average of 11 percent, according to the report. To read more go to http://tinyurl.com/c7ahmjg

Baby Boomers Aren’t Retiring

In huge numbers, members of the baby boom generation — born from 1946 through 1964 — tell researchers that they don’t plan to retire. In one recent AARP survey, nearly 70 percent of baby boomers reported they intend to work past the traditional retirement age of 65. Some like their work, but many simply can’t retire. Read more here: http://tinyurl.com/d52fj4d.

Middle Class Retirement at Risk

According to an AARP study, “many of today’s middle-class workers — especially those in their 20s, 30s, 40s and 50s — will not have a middle-class retirement. In fact, 30 percent of those currently in the middle class will become low-income retirees. This middle-class squeeze is not just a challenge for the 50-plus population of today; it’s also a challenge for the 50-plus population of tomorrow.” Read more at http://bit.ly/14kRGKz. You can also find it on our Facebook page.

Now That’s What I Call a Pension

“After retiring from a 36-year career in the U.S. House of Representatives last month, Norm Dicks (now working as a consultant with defense companies) has no doubt that he’s worth every penny of his new pension: It will allow the Washington state Democrat to cash a monthly check from the U.S. government for $7,365.82. That’s the net pay on his gross annual pension of $107,268, or $8,939 per month”.

How many of us put in a 35 year career with the state for a 40,000 pension and Michigan thinks they are being robbed. Read more here: http://tinyurl.com/clxfcfs

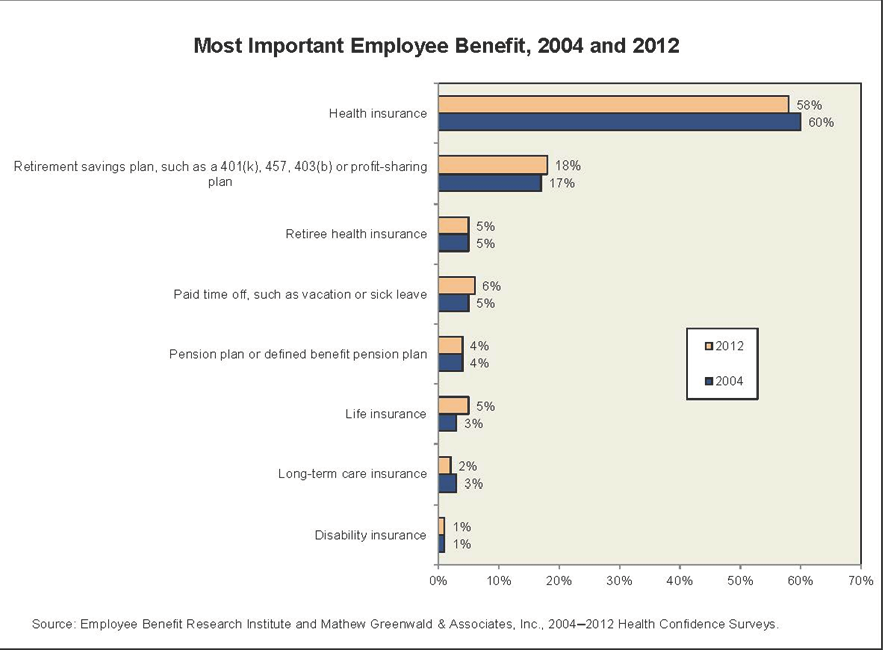

Benefits Still Very Important to Employees

AARP and Northwest Initiative Project

AARP Michigan and the Northwest Initiative commissioned a mail survey of Lansing residents to help map out current and future personal needs as well as interest in a Lansing Village in order to provide a direction for the future. In 2010, one in three Lansing adults (33% or 38,200 residents) was age 45 years or older. When asked to rank in order of importance the eight types of services residents would need now and in the future, Home Maintenance, Health Assistance, and Daily Living Services were the top three ranked types of services. Older populations overwhelmingly prefer to receive services and supports within their homes or communities. To read more about the survey and its findings go to http://tinyurl.com/ckv9qdo

Was it Ethical?

State employees were led to expect that after an established number of years, a certain level of retirement security would be available to them in retirement. The Michigan Supreme Court has ruled (erroneously in my opinion) that the promises were not legally binding. In any event, state workers made personal decisions based on these expectations, such as how much additional money to save over the years to supplement their pension. It was unethical of past officials to make pension promises that depended on forever-booming revenues and not set aside enough current revenue. People are elected in hopes they will use good judgment and common sense in determining state policies. However, it is apparent that elected officials who make funding decisions were not well versed in the economics of the stock market or the ethics of keeping their word. Read the article from Kiplinger Magazine at www.kiplinger.com/article/business/T020-C013-S001-is-it-ethical-to-breark-pension-promises.html#9ScrcqhLBhpxoa63.99

How Healthy is Michigan?

“The Gallup-Healthways Well-Being Index, which has surveyed 1.7 million Americans since the survey was first conducted in 2008, reflects the physical and emotional health of residents in each of the 50 states. On top of calculating an overall national level of well-being, the index also calculates the well-being for each state, assigning scores from 0 to 100, with 100 representing ideal well-being.

Here is the ranking for Michigan:

36. Michigan

- Well-being index score: 65.6

- Life expectancy: 77.9 years (17th lowest)

- Obesity: 28.5% (15th highest)

- Median household income: $45,981 (17th lowest)

- Adult population with high school diploma or higher: 88.8% (22nd highest)

Michigan underperformed the country’s average scores in nearly all of Gallup’s categories used to measure well-being. The state received especially poor scores in physical health, with residents more likely to report recurring pain in their neck or back, their knees or legs, or elsewhere. The state also rated poorly in the emotional health category, with residents more likely to report feeling disrespected or stressed. Among possible contributing factors to low physical and emotional health ratings could be the higher than average rate of smokers in the state and the very low rate of job satisfaction. Michiganders also had among the highest unemployment rates in the country as of December 2012.” Read more: www.well-beingindex.com/files/2013WBIrankings/MI_2012StateReport.pdf

Impact of Michigan Tax changes

Many Michiganders are just now feeling the impact of the 2011 tax shift. Many of these changes went into effect at the beginning of 2012, just in time to file their 2012 taxes. The Associated Press provides a rundown of the ways in which the tax bills of typical Michiganders will look different from previous years. The Institute on Taxation and Economic Policy (ITEP) estimates that changes in the personal income tax would result in tax increases of $100 for a poor family, $300 for a middle income family and $7 for a rich family. Read more at http://tinyurl.com/cskv9hz

NOTE TO READERS:

I know some of the web site addresses given in my article are long and cumbersome at times. I have tried to use the shortened version of the address but as I test my links, if they don’t work for me I leave the real URL (address) in the article. Please bear with me as I try to find a solution to the long URL issue and why some of the shortened versions don’t always work. In the meantime, you can copy and paste the address in your browser rather than try and copy it down on paper. However, if your don’t get your newsletter electronically, and therefore, must copy it down, try using a key phrase from the article to see if you can locate the story. I understand that long URLs are a problem. Thanks for your patience and I truly appreciate all the kind words about the Pension Report.

Editor’s note: June Morse may be contacted at jmorse10@comcast.net or 517-886-9323.

Return to top of page