Pension Matters

State Employees Retirement Fund

Most Recent Market Value | Archived Monthly Profiles

October 2012

Investment Advisory Committee Meeting

At the September 6th Committee meeting, Mr. Braeutigam gave the Executive Summary which included the MPSERS plan annualized return of 2.6% for the past one year, 11.5% for a three year period, 1.4% over a five year period and 6.2% of a ten year period. Domestic equity allocations have been reduced by 6.7% over the past 12 months and short term cash was increased by 2.6%.

Much of the meeting time was given to a presentation by RV Kuhns Associates on the “Asset/Liability, Investment Strategy (for MSERS) and the Wind Down of a Closed DB Plan”. The purpose of the study is to “examine future consequences over extended periods of time and applying alternative asset allocation plans to the investment assets.

Two major themes emerged from the study’s conclusions:

- Despite MSERS’ mature population, this System’s financial health is likely to improve over the next 20 years.

- The investment strategy will move toward a lower volatility asset allocation.

As of September 30, 2011, the System’s market value funded ratio was 56% and an actuarial funded ratio of 65.5% As a closed system, retirees drawing benefits currently exceed active, contributing members more than 3 to 1. While a few other public retirement funds have reduced the ROR from 8% to 7 1/2 or 1/4, this was not viewed as a key fundamental. Maintaining the ARC or increasing it, was viewed as critical by the consultants. The entire report can be viewed on the Bureau of Investment website at www.michigan.gov/documents/treasury/AssetLiabilityStudy_StateEmployees_368378_7.pdf

Reminder: The full reports from the Investment Advisory Committee Meetings are on line at http://michigan.gov/treasury/0,1607,7-121-1753_37621---,00.html

Take a look at what the Academy of Actuarials says about the 80% funding level.

“A funded ratio of 80% should not be used as a criterion for identifying a plan as being either in good financial health or poor financial health. No single level of funding should be identified as a defining line between a “healthy” and an “unhealthy” pension plan. All plans should have the objective of accumulating assets equal to 100% of a relevant pension obligation, unless reasons for a different target have been clearly identified and the consequences of that target are well understood.” Read the entire brief at www.actuary.org/files/80%25_Funding_IB_FINAL071912.pdf

New Retirement Board Member

New employee member appointed by the Governor is Ruth Duquette, a DTMB employee in management was introduced at this month’s retirement board meeting.

401K Fee Study

At the end of 2010, employer-sponsored defined contribution plans held an estimated $4.5 trillion in assets, and for many American workers, these plans have become an important part of retirement savings. As assets in defined contribution plans have grown, so too has the scrutiny around these plans. The fees charged for these plans have come under particular focus as the Department of Labor (DOL) wants to create greater transparency through regulatory disclosure requirements under sections of the Employee Retirement Income Security Act (ERISA). As part of its research program, the Investment Company Institute and Deloitte Consulting LLP have prepared a second edition of the “Defined Contribution/401(k) Fee Study” that was first published in 2009. This report addresses and updates the mechanics of defined contribution plan fee structures, components of plan fees, and primary and secondary factors that impact fees. The full report is at http://tinyurl.com/8pumoxo

Interesting Article

In a new report, the National Association of State Retirement Administrators (NASRA) notes that pension spending levels for states and cities vary from the national average: from less than 1 percent to more than 6 percent. It also says that most of the variation in pension spending levels is attributable to three factors: different levels of effort by states and cities to make pension contributions; differences in benefit levels; and variations in the size of unfunded pension liabilities. As a percentage of total spending, pension costs for cities are higher than states by about 50 percent. For more information go to www.nasra.org/resources/NASRACostsBrief1202.pdf

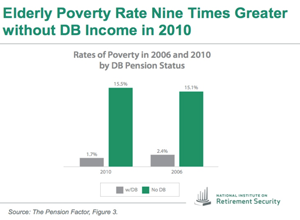

Poverty Risk Increases 50 Percent For Older Americans Lacking Pensions

Rates of poverty among older households lacking defined benefit (DB) pension income were approximately nine times greater than the rates among older households with DB pension income in 2010, up from six times greater in 2006. Older households with lifetime pension income are far less likely to experience food, shelter, and health care hardship, and less reliant on public assistance. The data also indicate that pensions are a factor in preventing middle class Americans from slipping into poverty during retirement.

Rates of poverty among older households lacking defined benefit (DB) pension income were approximately nine times greater than the rates among older households with DB pension income in 2010, up from six times greater in 2006. Older households with lifetime pension income are far less likely to experience food, shelter, and health care hardship, and less reliant on public assistance. The data also indicate that pensions are a factor in preventing middle class Americans from slipping into poverty during retirement.

The Pension Coverage Problem in the Private Sector

Another paper from the Center for Retirement research at Boston College states that only 42 percent of private sector workers age 25-64 have any type of pension coverage in their current job. This gap creates two types of problems, l) more than a third of households end up at retirement with only Social Security and 2) workers who move in and out of coverage accumulate only modest amounts in their 401(k)s. To read the paper go towww.crr.bc.edu/briefs/the-pension-coverage-problem-in-the-private-sector/

And yet...

Public pensions that are available in the private sector seem to be doing well. Pensions&Investments, an international newspaper for money management, collected defined benefit fund information from the annual reports of companies in the Dow Jones Global Titans index, including commentary and information on the plan sponsors funded status, asset allocation and other key topics. Forty-four companies in the index had defined benefit plans with more than $802 billion in total assets. The data show the plans being “generally well funded; significant interest rate head winds; and a gradual shift into alternative investments.” Read more at www.pionline.com/assets/docs/CO8051279.PDF

Regulatory References

“The Governmental Accounting Standards Board (GASB) has published two standards it says are “intended to improve the accounting and financial reporting of public employee pensions by state and local governments.” Statement No. 67, Financial Reporting for Pension Plans, revises existing guidance for the financial reports of most pension plans, and Statement No. 68, Accounting and Financial Reporting for Pensions, revises and establishes new financial reporting requirements for most governments that provide their employees with pension benefits”. Both are available to download at no charge on the GASB website. http://tinyurl.com/7ozfo8u

Lawsuit to safeguard Michigan’s pension funds and protect current and future retirees?

Michigan has joined in a lawsuit “challenging a key provision of the Dodd-Frank financial reform law enacted in 2010.” The law’s supporters said the orderly liquidation authority was designed to give the government better options to deal with a repeat of the Lehman Bros. collapse in the fall of 2008, which triggered the financial crisis.

The attorneys general are joining as part of a broader suit against the Dodd-Frank law brought by State National Bank of Big Spring, Texas; the 60 Plus Assn., a senior citizen advocacy group; and the Competitive Enterprise Institute, a public policy group. The suit alleges the law granted the agency (the FDIC) too much power and that Obama’s recess appointment of Richard Cordray as its director was unconstitutional. The suit also says the law’s creation of the Financial Stability Oversight Council, a panel of regulators, is unconstitutional. Read more at http://tinyurl.com/9b9gb2b.

What to do with all that Money?

LANSING (WTVB) -“So what do you do when you find an extra $88 million dollars? In the case of the state of Michigan, you put it back into the Rainy Day Fund. According to State Senator Bruce Caswell, lawmakers later this month are scheduled to vote on a Negative Supplemental Bill that would return money saved from reforms in the state employees pension fund, revised building leases, and 352 vacant positions not being funded.

The state is also moving up a scheduled reduction of the states income tax from the end of 2012 to this October. That is reduction is from 4.35 percent to 4.25 percent.”

How about putting it toward unfunded liabilities?

Public Health Insurance growing

“WASHINGTONThe uninsured rate for working-age Americans ticked down in 2011, but only because public program coverage grew faster than employment-based health insurance coverage declined, according to a new report by the nonpartisan Employee Benefit Research Institute (EBRI).

While employment-based health coverage is still the dominant source of health insurance in the United States, it has been steadily shrinking since 2000. The latest data show that it continued to do so last year.” To read more go to, www.ebri.org/pdf/briefspdf/EBRI_IB_09-2012_No376_Sources.pdf

Notes Worthy from EBRI

“MEMBER SHIFTS. The share of American families with a member in any employment-based retirement plan from a current employer increased steadily from 38.8 percent in 1992 to 40.6 percent in 2007, before declining in 2010 to 37.9 percent. Ownership of 401(k)-type plans among families participating in a retirement plan more than doubled from 31.6 percent in 1992 to 79.5 percent in 2007, and increased again in 2010 to 82.1 percent. But while overall retirement plan participation by families declined from 20072010, the percentage of family heads who were eligible for defined contribution plans and chose to participate held essentially stable.”

MEDIMPACT UPDATE

“In talking with Employee Benefits today I have learned that they are not in a position to attend various SERA Chapter meetings at the present time to discuss the Prescription Drug Plan that will take effect on January 1, 2013. I have been assured that representatives from MedImpact will be flying in from Arizona just prior to the November 9th CC meeting to finalize the details of the Rx Plan. I have been informed that Employee Benefits, MedImpact, Office of Retirement Services are in the process of coordinating all the details that go into the Employer Group Waiver Plan and the secondary wrap-around to make sure the Rx Plan is as seamless as possible. There are no details that can be released at the present time. Please refrain from asking Employee Benefits to attend Chapter meetings to discuss the new Rx Plan. Their first full explanation will be to the Officers, Chapter Presidents and Delegates/Alternates that will be in attendance at the November 9th CC meeting. It is my intention that the business meeting will be concluded before lunch and that MedImpact and Employee Benefits will have the remainder of the afternoon to explain the Plan and answer questions.”

Bob Kopasz, Chair

SERA CC

Editor’s note: June Morse may be contacted at jmorse10@comcast.net or 517-886-9323.

Return to top of page